Understanding the nuances between subsidized loans and unsubsidized loans is crucial for anyone navigating the complex world of student financing. This guide is tailored for savvy borrowers who are well-versed in financial terminology yet need a deeper dive into these types of loans.

What Sets Subsidized Loans Apart from Unsubsidized Loans?

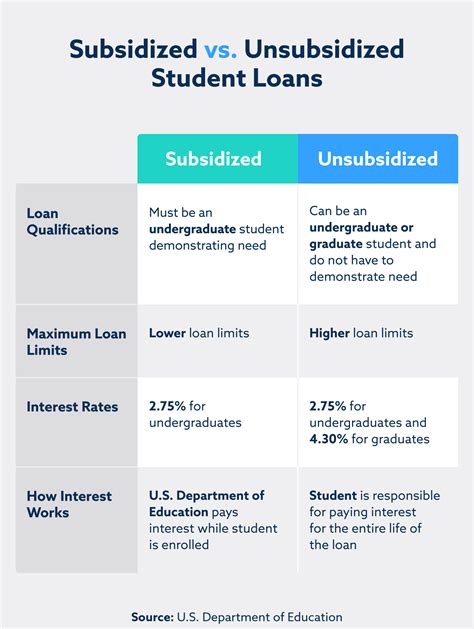

Subsidized loans are provided with financial support from the government to cover a portion of the interest that accrues while you’re in school. In contrast, unsubsidized loans do not receive this support, meaning you are responsible for the full interest that accrues at all times. This fundamental difference directly impacts your monthly payment and overall cost of attendance.

Key Insights

Key Insights

- Subsidized loans have interest paid while in school, reducing your overall cost.

- Unsubsidized loans accrue interest from the beginning, which can lead to higher payments.

- Choose subsidized loans if possible, as they often lead to lower long-term debt.

The Mechanics of Subsidized Loans

Subsidized loans, also known as Pell Grants, are funded by the government and come with significant benefits. The government pays the interest that accrues while you’re in school, as long as you maintain satisfactory academic progress. This means you don’t need to make any payments while you’re in school, during grace periods, or while you’re in deferment or forbearance. Additionally, the amount you can borrow is often capped based on your year in school and financial need.

One practical application of this type of loan is for students pursuing undergraduate studies. For example, a first-year student from a middle-income family could receive up to $6,495 in subsidized loans, which can cover a substantial portion of their educational expenses.

The Dynamics of Unsubsidized Loans

Unsubsidized loans do not have the government covering interest. This means that interest starts accruing immediately after you receive the loan, and unless you pay it off, it will add to your loan balance. This can lead to significantly higher payments once you graduate and begin repayment. While the borrowing limits are similar to subsidized loans, the key difference lies in the cost burden you assume.

For instance, if you receive a $10,000 unsubsidized loan, you will have to pay all the accrued interest. Should the interest rate be 4%, the interest alone would total $400 per month. Over four years, this adds up to $19,200. In comparison, a subsidized loan for the same amount with the same interest rate would see only the principal repaid, as the government covers the interest while in school.

FAQ Section

Are there any income limits for subsidized loans?

Yes, income and financial need play a significant role in determining eligibility for subsidized loans. Typically, students from lower-income families have a higher chance of qualifying for these loans.

What happens to unsubsidized loan interest if I stop making payments?

If you stop making payments on an unsubsidized loan, the interest will continue to accrue and will likely become capitalized, adding to your principal balance. This can increase your future monthly payments significantly.

Choosing between subsidized and unsubsidized loans requires careful consideration. Subsidized loans often lead to lower long-term debt due to government-covered interest while in school. For the most financially savvy borrowers, understanding these differences can make a significant difference in their financial outcomes. Whether you’re just beginning your journey or deep into your educational program, grasping these concepts can lead to smarter financial decisions and reduced overall debt.